If you run a contact center for a UK financial firm, FCA compliance now lives on your phone lines.

The Consumer Duty raises the bar for everyday conversations. You must prove your service helps customers reach good outcomes, not just avoid bad ones.

The Duty applies to open products since 31 July 2023 and to closed products since 31 July 2024.

That shift puts customer support and, therefore, your call center under sharper scrutiny.

The numbers show why it matters.

Firms reported 1.78 million complaints to the FCA in H2 2024.

The Financial Ombudsman Service (FOS) received 305,726 new complaints in 2024/25, the highest in six years. Your call center sits at the front line of those journeys.

This guide breaks down what the FCA expects from call centers, what rules bite hardest on the phones, and how to design operations, metrics, and training that satisfy the Duty every day.

A. What is FCA compliance?

The FCA protects consumers and markets. It oversees tens of thousands of financial firms. Its goal is fair treatment, honest communication, and competitive markets.

It expects you to deliver good outcomes, not just meet checklists. That’s the spirit behind the FCA Consumer Duty.

Here are the core objectives your teams should live by daily:

- Fair treatment. Customers should get suitable products and advice. Pushy sales don’t cut it. Products must fit needs and risk appetite.

- Transparency. Communications must be clear, fair, and not misleading. No hidden fees. No sugar-coated promises. No confusing jargon.

- Complaint handling. Treat complaints as signals. Investigate well. Resolve fairly. Learn and fix root causes.

- Vulnerable customer protection. Some customers face a higher risk of harm. Age, health, bereavement, debt, or low capability can increase risk. You must spot vulnerability and adapt your service accordingly.

- Record keeping. Capture and keep relevant communications. For many activities, the Handbook requires recording phone conversations and storing them. That lets you evidence what was said later.

Why are call centers the biggest risk area?

Because they are the frontline, agents must communicate complex terms, assess needs, and show empathy in minutes.

They must follow FCA regulations precisely while juggling systems and stress. This is where FCA quality monitoring matters most.

It’s also where errors hide if you only sample a few calls.

History proves the stakes.

The PPI scandal paid more than £38.3 billion in redress. Much of that stemmed from mis-selling in conversations. It’s a powerful lesson for modern operations.

B. Why compliance is tough in call centers

High volume, low visibility. You take thousands of calls monthly.

Traditional QA listens to a tiny slice. Many centers review about 1% of interactions.

That leaves a huge blind spot. Issues go unseen until complaints pile up.

- Human pressure. Agents chase targets and handle queues. Fatigue and stress cause slips. A missed APR disclosure. A rushed eligibility check. A promise that sounds too certain. None of that is malicious. It’s the reality of a busy floor.

- Training gaps. Rules evolve. The Consumer Duty changed expectations. New starters rotate in. Veterans pick up habits. Without constant reinforcement, scripts drift. Small drifts cause big compliance gaps.

- Mis-selling risk. Sales language can creep past “clear and fair.” The lessons from PPI are vivid. Missed needs assessment. Weak explanations. Customers are confused or mismatched with products. That history still shapes the FCA mindset today.

- Complaint handling under strain. Fast “defuse and close” behaviors can emerge. The HomeServe case is a stark example. The firm was fined £30.6m for mis-selling and poor complaint handling. Incentives pushed speed over fairness. The regulator took notice.

- US customer stakes are high. One bad experience can trigger churn. 32% of US customers leave a brand they love after a single bad interaction. Multiply that by hundreds of calls a day. The cost of one poor disclosure or tone mistake becomes clear.

C. FCA expectations vs. call center reality

The gap is real. Here’s a quick reality check you can share with leaders.

| FCA Wants | Call Center Risks |

| Fair treatment. Match products to needs. No pressure tactics. | Sales pressure. Quotas can nudge agents toward mis-selling behaviors. |

| Transparency. Clear, fair, not misleading. Key terms and fees explained. | Missed disclosures. APR, fees, and exclusions get rushed or skipped by mistake. |

| Support for vulnerable customers. Identify, adapt, and protect. | Rushed handling. Agents miss cues like confusion, bereavement, or hardship. |

| Robust records. Capture calls and keep them. Show what was said. | Scattered notes. Sampling hides problems. Poor audit trails weaken evidence. |

| Effective complaints process. Investigate, fix, and learn. | Close fast mindset. Escalations missed. Incentives can skew behavior. Regulatory risk follows. |

Bridging this gap needs scale, speed, and consistency. That’s where automated QA for call centers pays off.

D. How AI QA helps ensure FCA compliance

Here’s how AI QA turns compliance from guesswork into proof at scale.

- Monitor 100% of calls. AI transcribes and analyzes every conversation. No more 1% sampling. No more guesswork. You get full coverage across teams, products, and partners. The benefit is simple. You see the true risk picture, not a tiny slice.

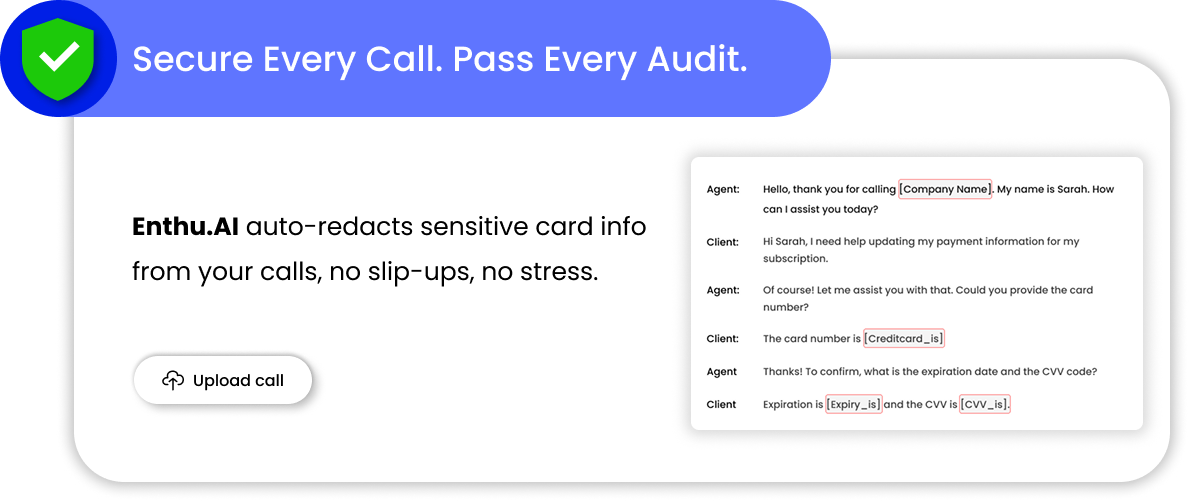

- Automated disclosure checks. Configure the required language for your products. Watch for APR mentions, fee explanations, cooling-off terms, and identity verification. The system flags any miss instantly. You review targeted snippets, not full recordings. That saves time and lifts accuracy.

- Detect vulnerable customers. AI looks for keywords and patterns that signal vulnerability. Words like “bereaved,” “ill,” “lost job,” or “confused” stand out. Sentiment and pace also matter. When flagged, supervisors can verify care and follow-up steps. That maps to the FCA guidance on protecting those at risk of harm.

- Complaint detection and escalation. Not every complaint uses the word “complaint.” AI spots frustration spikes, demand for managers, or phrases like “this is unacceptable.” It tags potential complaints automatically. That helps you log, track, and resolve issues effectively. It also builds a clean audit trail for DISP reviews.

- Evidence for regulators. The FCA expects you to evidence outcomes under the Consumer Duty. AI-generated transcripts, time stamps, and compliance scorecards make that easy. If the FCA asks, you can pull the exact call and highlight the exact disclosure. You move from scramble to audit-ready.

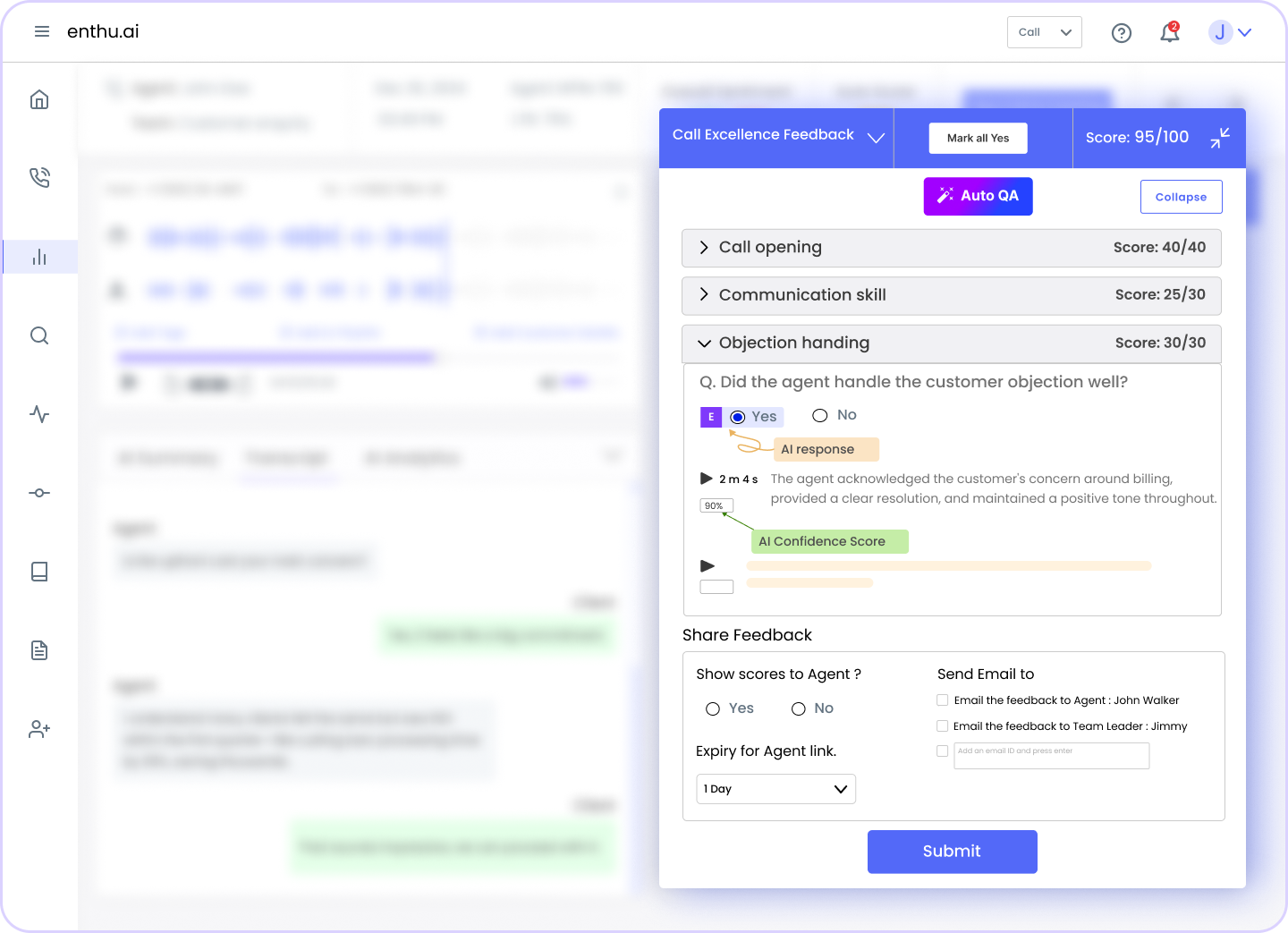

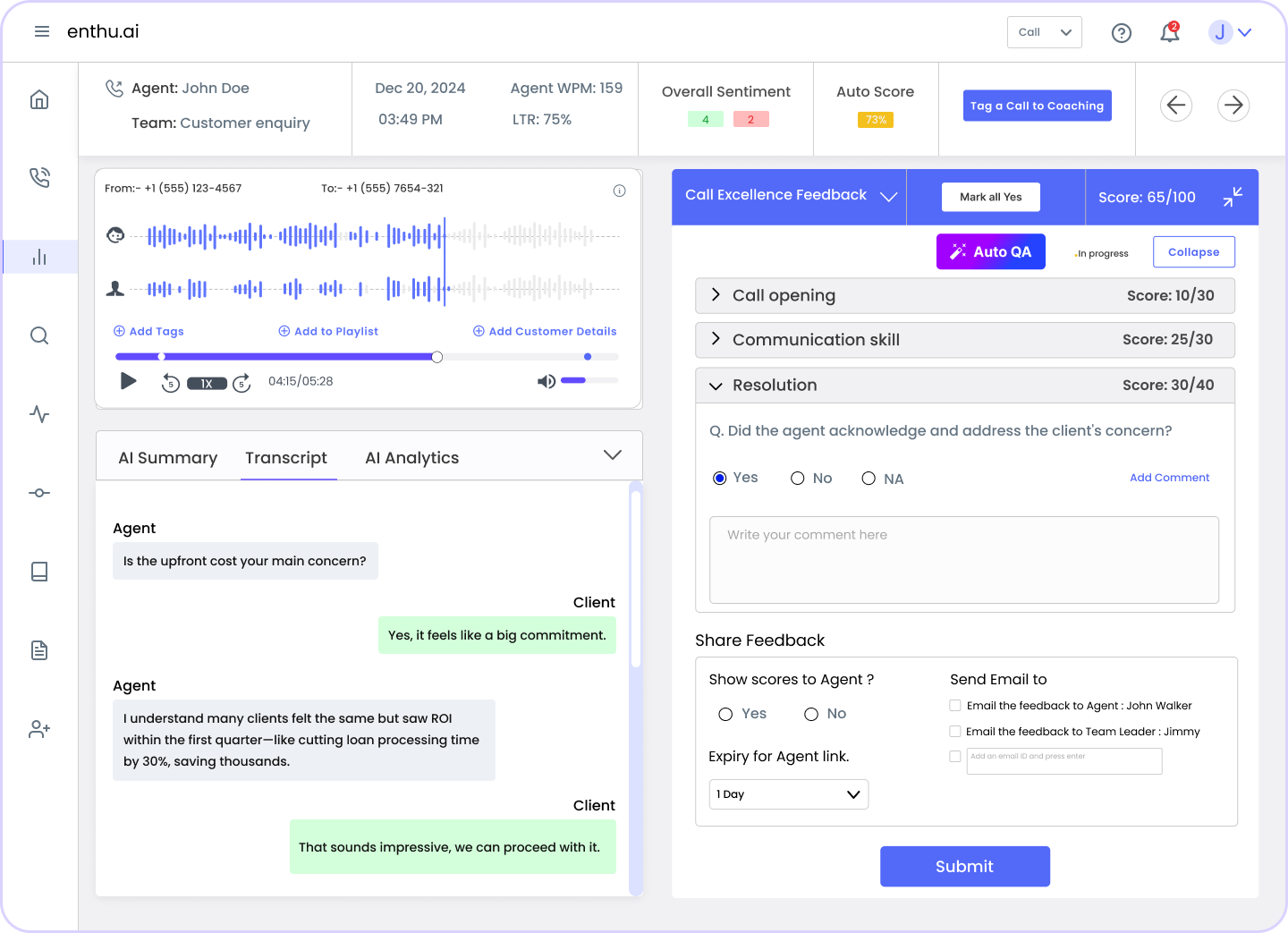

- Real-time coaching. AI can nudge agents live or near-live. “Mention APR now.” “Slow down and re-explain fees.” “Offer alternative support.” After the call, AI-powered coaching for agents provides focused feedback. Leaders coach to patterns, not hunches. Over time, behaviors shift, and breaches fall.

- Find and fix patterns early. AI surfaces trends across teams and products. Maybe a new loan script creates confusion. Maybe one region misses ID checks more often. You spot it fast. You adjust scripts, training, or controls before customers are harmed.

Case study: Avoiding mis-selling in loans

A regional lender sold unsecured loans over the phone. Manual QA covered about 1% of calls. Missed fee disclosures flew under the radar. After deploying AI, they monitored 100% of calls. The system flagged where agents skipped the total cost explanation. Managers coached those agents within 24 hours. Within six weeks, disclosure accuracy rose from 82% to 98%. Complaint volumes on lending calls fell 22% quarter-over-quarter. The lender avoided a potential wave of refunds and reputational hits. The team now reports Consumer Duty metrics to the board with confidence.

E. Why Enthu.AI is the compliance partner you need

Here are the ways Enthu.AI makes FCA compliance practical – turning every call into audit-ready proof, faster coaching, and fewer risks.

- Built for financial services QA. Enthu focuses on banks, lenders, and insurers. Our FCA quality monitoring scorecards include identity checks, disclosures, affordability cues, and prohibited phrases. You get meaningful signals from day one, not months later.

- Automated scoring at scale. Enthu analyzes every call. It scores adherence to FCA regulations and your internal policies. Missed items are flagged with time stamps. Your QA team reviews what matters. That saves hours and boosts consistency across analysts.

- Searchable transcripts and clean audit trails. Every call is AI transcribed and indexed. Need to find all “early repayment fee” mentions last month? Search and go. Preparing for an internal audit? Export transcripts and scorecards with a click. Need to show your Consumer Duty monitoring outcomes? You’re ready.

- Real-time alerts and workflow. Enthu routes high-risk calls to supervisors instantly. Think failed ID&V, missing APR, or potential vulnerability. Leaders get context and snippets, not a pile of audio. Follow-ups get tracked to closure. That’s true call center compliance monitoring.

- Coaching that actually sticks. Enthu turns findings into personalized coaching tips. Leaders get talk tracks and examples pulled from real calls. Agents see what “good” sounds like. Coaching becomes faster, fairer, and data-driven.

- Faster, safer, and cheaper. Avoid fines and rework. Reduce manual listening time. Protect your brand. Lift NPS and CSAT by removing friction and confusion. The business case is simple. One avoided breach can fund your QA program for years.

Try it with zero risk. We’ll run 5 free evaluations on your recordings. See your own data. Spot quick wins in a week. If you like what you see, scale it. If not, you still gain insight.

Conclusion

Regulation isn’t going away. Standards are rising with the FCA Consumer Duty. Customers expect empathy, clarity, and fairness.

Your contact center sits at the crossroads of all three. You don’t need to choose between speed and safety. With the right stack, you get both.

AI lifts visibility from 1% sampling to every call. It finds risks fast. It creates proof for auditors. It helps your people do the right thing, consistently.

Enthu.AI makes this practical. It’s purpose-built for financial services. It watches every conversation. It flags what matters. It helps you coach and comply, day after day.

That’s how you protect customers and your brand.

FAQs

1. What does the Consumer Duty change for call centers?

It raises expectations. You must prove customers get good outcomes. That means clear language, suitable products, and strong support. It also means better evidence. Transcripts, scorecards, and case logs help you show your work. The Duty has been in force for most retail products since July 31, 2023. Closed products followed in 2024.

2. Do we really need to record and store calls?

Yes, for many regulated activities. FCA rules require firms to record phone conversations and keep them. This supports investigations, complaint reviews, and audits. Strong record keeping protects customers and the firm.

3. Why not stick with manual QA sampling?

Because it misses too much. Many centers review around 1% of interactions. That leaves risks undetected until customers complain or the FCA asks questions. AI lets you review 100% of calls. You get scale, speed, and consistency.